Homeownership: Is a High Homeownership Rate Good Policy? No. Examining 3 Cycles of Homeownership Data over 100 years and Implications for the Economy.

- 0 Comments

The current housing crisis has left us with an opportunity to examine the driving issue behind a high homeownership rate. Is it really worth it to push for an economic policy that champions a high homeownership rate? The problem with blanket statements is they usually play into herd mentality and feed into group think. One of the statements we have lived with for the past decade is “everyone should own their own home.” Such statements mask a three decade long housing bubble and also don’t research the basis for economic sustainability.

The problem with pushing a pro-housing agenda is it covers up a lot of other sins. For example, owning a home with a conventional mortgage that you can afford is in most cases a good thing. But is it worth it to purchase a home where most of your money is going to pay for the mortgage, which is a financially dangerous option ARM like many now have? When you start cutting deeper into the analysis, you realize that homeownership for all is simply a populist rallying cry.

From 1900 to 1930 the homeownership rate remained flat around 43 percent. Rates shot up during the 1940s and 1950s during the baby boom:

If we look at data for over 100 years of U.S. homeownership rates we see 3 major cycles. First, from 1900 to 1930 we see a generally stagnant growth rate. Mortgages also had stricter terms:

“As the U.S. economy contracted, loan delinquencies and foreclosures soared, fueled by falling household incomes and property values. Many home loans had terms of five years or less and often involved no, or only partial, payment of principal before a balloon payment was due when the loan matured or was refinanced. Refinancing was common and easily accomplished in the 1920s, an environment of rising incomes and property values, but next to impossible during the Depression. Falling incomes made it increasingly difficult for borrowers to make loan payments or to refinance outstanding loans as they came due. The failure of thousands of banks and other lenders contributed to the difficulty of refinancing, as customer relationships were severed and the costs of credit intermediation rose.”

-Federal Reserve Bank of St. Louis, David Wheelock

We should first acknowledge what was similar during the Great Depression and our current crisis. First the similarities:

(a)Â Refinancing was good so long as the economy was rising.

(b)Â Once incomes fell and the depression hit, refinancing was nearly impossible.

So housing was on a much quicker revolving timeline with 5 year mortgages. More people also paid off mortgages quicker. Let us now highlight some clear differences:

(a) Homeownership stayed around 43 before and after the Great Depression. Our peak homeownership rate hit in 2004 and was at 69.2 percent.

(b)Â Mortgages have longer terms.

Those are some stark differences. The Great Depression did put some pressure on home values but you’ll notice that the lull during this time was not that significant. Rates remained above 40 percent even during the worst times of the depression.

The next phase is the baby boom phase. This was the largest increase in the homeownership rate that the country has ever seen and spanned two decades. First, when families formed and then, when the baby boomers went out and started their own families. You had a two wave here. In addition, during the Great Depression Fannie Mae was established which provided more generous and accommodating mortgages. This may be the only time that we have seen a major spike that had a legitimate case in demographics.

The final cycle which was our current housing bubble which has seen $50 trillion in global evaporate, was driven in large part by a credit bubble and a mania in virtually every asset class but in particular, real estate. You’ll notice on the chart above that this pushed the homeownership rate from approximately 64 percent to 69.2 percent. Most of those gains have now disappeared because much of the new homeownership gains were based on sub-prime, Alt-A, and other toxic mortgage products that were only workable so long as housing prices continued to go up.

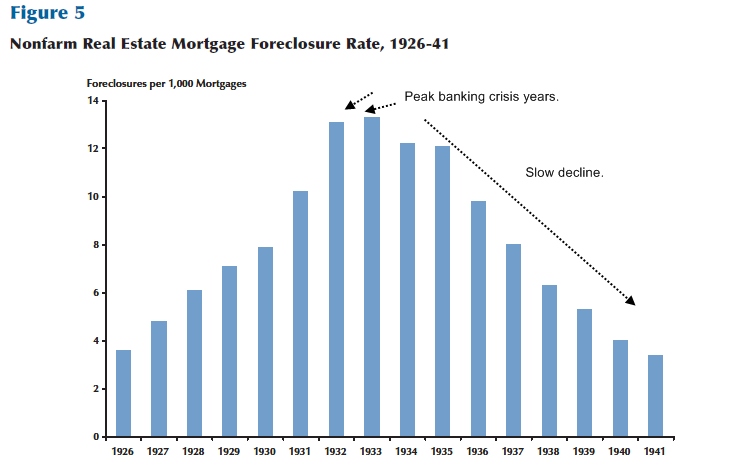

Homeownership isn’t good or bad. It is a necessity we all have. In some areas of the country it is more important to focus on affordable housing and by definition the housing bubble with prices reaching the stratosphere went contrary to this nationwide aspiration. We do have a crisis not with housing shortages but with affordable housing. Putting people into dangerous mortgages during hard economic times simply does not make sense. Take a look at the foreclosure rates during the Great Depression:

What you’ll notice is that foreclosures peaked during the banking crisis years. Keep in mind that the market crashed in 1929 and foreclosures didn’t peak until 1933, almost 4 years later. Our markets tanked in 2008 so if a similar pattern plays out, we can expect a peak in foreclosures in 2011 or 2012. Foreclosures are still on a path upwards and most analyst expect 2009 to be the worst year on record. We can expect continued market volatility as many retailers trim down and many people find themselves out of work and unable to service their mortgages, many of which will have higher payments.

So we go back to the idea that everyone should be a homeowner. I would argue that this shouldn’t be a national economic policy goal. What we should concern ourselves with is having a sustainable economy first. Only then, will people choose to pursue homeownership if they wish to do so. And why should we punish people that don’t choose to own? Currently, renters subsidize a portion of the homeowner mortgage tax deduction since renters receive no benefit from their shelter in terms of taxes. So by this action alone, we as a society are placing too high of a value on homeownership. We got carried away this decade and unscrupulous lenders and Wall Street created the environment for a once in a lifetime bubble that has hurt many families.

The Federal Reserve and U.S. Treasury would like Americans to go back to their spending ways of this decade yet that is simply not feasible. After all, we all acknowledge that it was a bubble so going back to the heyday would simply be admitting that we want to re-inflate the asset bubble. What we need is a sustainable nationwide housing mentality and this means that the homeownership rate will continue to decline. For those who want to be homeowners, they will still be able to do so with more modest terms, a bigger down payment, and actually having to wait maybe one or two years before taking the keys from the bank. Is that too much to ask?

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!