Is Oil Having an Impact on Housing? Taking a Look at Los Angeles County.

- 1 Comment

High gas prices are nothing new to those that live in Southern California. But there is something surreal about seeing prices quickly approach $5 per gallon. In fact, as you scroll through the list of your local gas station options, you’ll already see $5 a gallon for diesel serving as a highlight of coming attractions.

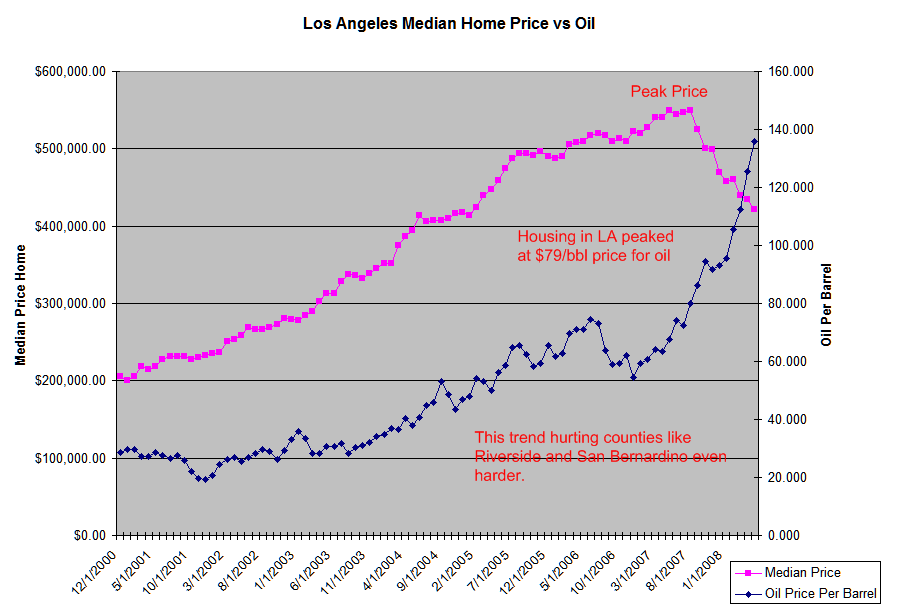

Has high energy prices impacted the price of homes? We were already having a housing bust before prices even started to decline. The Los Angeles median home peak price hit when oil was $79 a barrel:

(click for sharper image)

Of course, as typical in any economy, unintended factors normally impact other sectors without the benefit of foresight. It was hard for the travel industry to see online businesses such as Expedia or Travelocity take out a major chunk of their business. It was also challenging for newspapers to compete with online classifieds like those provided through Craigslist.

The idea of Peak Oil isn’t something that is new. In fact, the theory has been floating around for decades. Yet this may be the real deal. The fact that oil has stayed over $100 a barrel since January of 2008 only signifies that something radical may be happening. The world consumes over 84 million barrels of oil a day. Over 20 million of that is in the United States alone. Growing economies like those in China, India, and Russia are now consuming more and more oil so there is a true demand that is pushing prices up. Peak oil doesn’t mean we’ve ran out of oil but it simply means global production and refining capacity can no longer keep up with worldwide demand.

Prices in Los Angeles County are now down 23% on a year over year basis. It may come as no surprise to many that those in Los Angeles drive a lot. It is also no surprise that prices in Los Angeles are some of the highest in the nation. Take a look at the current average per gallon:

Today 4.572

Yesterday 4.581

One Week Ago 4.602

One Month Ago 4.160

One Year Ago 3.085

*Source: Gasbuddy.com

Higher gas prices are only contributing as an additional source for falling housing prices. More money is now being consumed on fuel and is allowing for less discretionary spending. Home prices in counties like Riverside and San Bernardino are taking it doubly on the chin with higher fuel prices. Many working class families with the hope of owning a home moved out into these areas and commuted into Los Angeles County to work. Now, this is not an option for many. That is why prices in these counties are now down by:

Riverside: -28.6% ($290,000)

San Bernardino: -30.8% ($250,250)

A few years ago, a home for under $300,000 in Southern California was almost unheard of. Now, this is a common occurrence. If fuel prices are to remain at current levels, it is only a mathematical certainty that people will be unable to commute from such long distances. Just to do some basic math, we’ll contrast $2 a gallon gas with the current $4.57 a gallon gas. Many people would commute 60 miles each way from San Bernardino to Los Angeles County to work. Let us assume they were driving a truck that could get 17 MPG:

120 miles per day

600 miles per week

Cost for week of gas (35.29 gallons needed):

@ $2 a gallon: $70.58

@ $4.57 a gallon: $161.27

Do this a few times over a month, and you are now spending $400 to $500 more a month while your income has remained the same. Now imagine this family in an adjustable mortgage which was extremely popular here in California. Now, you have rising fuel costs and a rising housing payment while the economic situation is deteriorating quickly in the state. This is strike one, two, and three.

Unfortunately this is simply adding fuel to the housing pain. Expect things to continue for the foreseeable future.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!1 Comments on this post

Trackbacks

-

riathareja said:

Rising interest rates and a falling demand may dent the realty market in India. However, the long-term prospects for the sector continue to be good, feels the industry. There are around 21 India-dedicated real estate funds that are raising money in the international market. In the next nine months, nearly $7 billion will be entering the country through various India-dedicated funds. While long-term players are looking at India, short-term players based in the US and Europe, such as the hedge funds and private equity players, are more interested in their local markets.For more view- realtydigest.blogspot.com

June 30th, 2008 at 11:10 pm