Two-thirds of Americans don’t understand how credit cards work: The debt addiction in your pocket.

- 5 Comment

There is something alluring about swiping a card and making a purchase. It almost seems euphoric and fun. Credit cards come in a variety of sleek designs to help you part with your current and future income. Americans are deeply in debt. Mortgages, student loans, auto debt, and credit cards consume a large portion of future income. You would think that most people would reflect on the mechanics of how debt works but this is not the case. Most people are oblivious to how credit cards work but continue to use them and go into deep debt. Throw in online shopping and you can store your credit information virtually and shop with one-click. This wouldn’t be such a problem if incomes were moving ahead. Unfortunately that is not the case and many are struggling to find their economic balance in the new low wage economy. Credit card debt is once again on the rise and two-thirds of Americans do not understand how credit cards work.

Don’t leave home without understanding

People spend more with credit cards. It is easy to understand. First, the convenience factor makes it much easier to blow through larger sums of money. Yet the bigger issue is having the ability to spend money you don’t have today, thus circumventing the need to budget to buy something. Take a look at some research regarding how people perceive value when spending cash versus credit:

“(The Atlantic) Prelec and Simester’s findings downplayed the importance of logos, but further solidified the theory that credit cards extract more money from people than cash in identical circumstances. The two researchers found that their Boston-based experimental subjects were willing to pay strikingly different amounts of money on tickets to a Celtics game, depending on their method of payment. Those paying with cash found roughly $30 to be a reasonable price, while those paying with credit on average were satisfied with $60. This Celtics experiment suggests that the premium is largest and most dangerous when people are making one-off purchases or buying things with uncertain value.â€

That is a big issue. Another study found that two-thirds of Americans don’t even understand how credit cards work. This should give you pause given the recent rise in credit card debt after a slumber from the Great Recession:

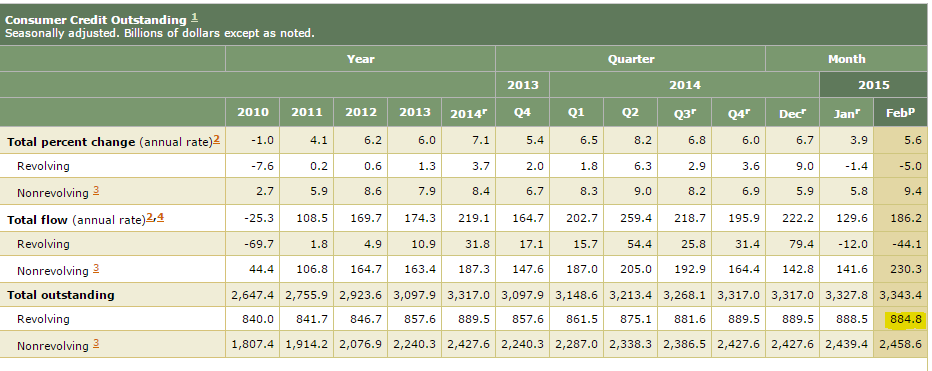

From 2010 to 2014 outstanding credit card debt remained fairly stagnant. In the last year it has started to trend higher at a quicker pace. The volume of credit card offers increases in tandem with the stock market and the overall perception of the employment landscape. Offers are now being pushed lower on the financial food chain since demand for other avenues of investments pick up. This is why we are witnessing a large push of subprime auto debt.

There isn’t anything inherently bad with credit cards. But the way they are marketed and the terms offered really lure people into spending money they don’t have on items they don’t need. Two-thirds of Americans don’t even understand how credit cards work! And then we wonder why half of the country has no money saved for retirement and most live paycheck to paycheck.

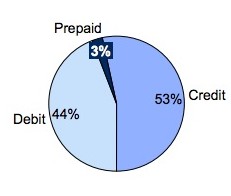

You might say that most of the non-cash transactions are coming from debit cards that pull from actual cash in checking accounts. Unfortunately most of the non-cash transactions occur in the form of credit cards:

The attraction is obvious and clear but the need for immediate gratification is going to be painful. Paying off a 60 inch television for five years is going to make you forget the high joy you get from that first year (or six months) of your purchase. Pretending to be rich is very different from being wealthy. In order to build wealth, you need to save and invest. Going into debt for things you don’t need is not wise financial planning.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! 5 Comments on this post

Trackbacks

-

Gilligan said:

A “credit card” is a debt card. The higher your points score the more debt you can acquire from the lender. This is usually based on how many assets you have, and how much income you make a year. You pay the lender interest for the privilege of borrowing money. He creates the money through a contract with you and the intent that you will pay it back.

April 24th, 2015 at 6:28 am -

btruth said:

I’d be willing to bet, that most DO know exactly how credit cards work, but with everything else that’s important, THEY DO NOT CARE!

April 24th, 2015 at 4:48 pm -

Rick Adams said:

A big amen to your last sentence. Some people just don’t get it. What’s that word I’m thinking of……….. oh yea, Sheep.

April 25th, 2015 at 3:28 pm -

Ame said:

Just a guess, but I would think many people who are using credit today are doing so in order to make ends meet, not for purchasing the appearance of being rich…at least that is what they SAY.

Wasn’t it here I read that wages have not risen since the 1970’s, yet the cost of living is up since then? Is it any wonder that Americans who work and bring home those wages fall in the credit trap? Especially when they watch so much tv. Television is filled with so-called “average folks”, but when you add up the cost of that lifestyle portrayed, you find those characters are actually living like upper class. The background sets in shows that portray normality all are nicely decorated. Who wouldn’t want to be considered normal? Poverty is portrayed with background sets using outdated furniture, etc. ( I use the example of tv shows because most everyone can afford to watch them.) America’s average citizen is supposed to be just like shown on tv, right?

The power of television shows and the commercials is what drives people. Would credit cards be so overused if tv were not available?

May 1st, 2015 at 4:04 pm -

Jon said:

They have been using the media since its inception to push their agenda’s, not just with assistance of creating a consumer economy, but with shaping politics, etc…

Watch The light bulb conspiracy | planned obsolescence-

https://www.youtube.com/watch?v=vfbbF3oxf-E

Or my favorite, The Corporation-

May 5th, 2015 at 9:51 am